Founders build. We clear the path.

We support you across the entire lifecycle.

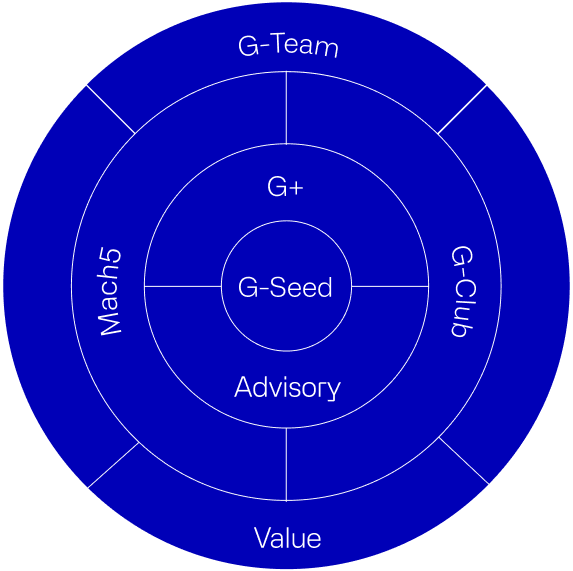

We built a full framework to back founders from seed to market leadership. One clear path with the right tools, people, and momentum.G-Seed starts it. G+ scales it. Mach5 accelerates it. G-Club surrounds it.Focused on Cybersecurity and AI, Glilot brings hands-on experience, flexible capital, and a global network that delivers results. We cover every stage with real, hands-on support.

G-Seed

Backs founders from first spark to scale. Early, deep, aligned.

G+

For founders ready to scale. Leads A/B rounds toward growth and dominance.

Exclusive wealth management for tech founders.

Value

We support founders with practical value, wrapping them with professional support from every possible type needed.

Five rounds of customer insight to hit product-market fit fast.

Fast access to top industry minds.

A VC that is deeply aligned with you - yep, that exists.

I love the Glilot team. They're incredibly professional.

Name:

Rotem Iram

Position:

CEO of At-Bay

Glilot helped us with every possible challenge, such as opening doors, hiring, and providing insights.

Name:

Daniel Krivelevich

Position:

CTO of Cider Security

Glilot is one of the most amazing VCs in cyber security.

Name:

Shay Morag

Position:

CEO of Ermetic

Glilot is founder-friendly and here to support founders and companies.

Name:

Yoav Levy

Position:

CEO of Upstream Security

IBM says newly published research demonstrates verifiable quantum advantage, with results that can be independently checked rather than just benchmarked. The findings, produced with partners including the University of Chicago, RIKEN and Qedma, mark a step toward using quantum systems for real scientific and business applications as IBM works toward a fault-tolerant quantum computer by 2029.

Knowledge-Hub

There are companies you become excited about because of the market, and there are companies you believe in because of the people. With Way Security, it was both.

When I first met the founders, I was struck by the depth of their thinking, the clarity of their ambition, and the way they approached a complex and crowded space with a genuinely fresh perspective.

They weren’t trying to build another identity point solution. They were asking a more fundamental question: what should identity security look like when the enterprise itself has changed?

That conviction led me to spearhead Way’s seed investment, and today I’m incredibly proud to see the company come out of stealth.

What made the opportunity so compelling wasn’t just the extraordinary quality of the team, but the scale of the architectural shift they had identified.

Identity Security Has Been Treated as a Collection of Separate Problems

For years, identity security has been treated as a collection of separate problems.

Organizations deployed one set of tools to manage workforce access, another to govern privileged accounts, another to monitor identity threats, and still others to manage cloud permissions, machine identities, contractors, and third-party access.

Each product addressed an important part of the identity problem. But the overall architecture remained fragmented.

That fragmentation was already difficult to manage. AI is now making it unsustainable.

Today’s identities are dynamic and that creates a fundamental mismatch between the identity infrastructure most enterprises have today and the identity reality they are being asked to secure.

This Is the Problem Way Security Was Created to Solve

This is the problem Way Security was created to solve.

Way Security starts from a truth most of the industry ignores: enterprises already own the right identity tools. What’s missing is not another product. It is the ability to enforce those tools on every application and every identity, including the legacy, homegrown, and non-standard systems where enforcement has always broken down. Way Security connects the IAM stack an enterprise already runs to the apps and identities it could never reach, and makes every control hold there: authentication, provisioning, governance, hygiene. Nothing replaced. Everything is enforced.

That’s not an incremental improvement. It’s a change in the operating model.

Why This Matters Now

AI doesn’t create the identity problem, but it dramatically accelerates it.

AI agents are being connected to enterprise systems, granted access to sensitive data, and allowed to act on behalf of users and business processes. In many cases, organizations don’t yet have a consistent way to understand what those agents can access, how their permissions interact, or what happens when their behavior changes.

At the same time, human and machine identities are becoming increasingly interconnected.

The distinction between workforce identity, workload identity, application identity, and agent identity is becoming less useful from a security perspective. Attackers do not care which organizational team owns a credential or which product manages an entitlement. They look for the path that gives them the reach they need.

Security architecture must evolve accordingly, and that’s the paradigm shift Way is building toward.

A Category Validated, but Not Yet Won

The emergence of additional companies lately in this space is meaningful validation.

It confirms that the market increasingly recognizes identity as a foundational layer of enterprise security. rather than a collection of isolated administrative workflows.

But categories aren’t won by huge marketing campaigns.

They are won through architectural clarity, product depth, customer trust, and the ability to turn an ambitious thesis into something security teams can deploy and rely on.

Why My Conviction in Way Is Especially Strong

This is where my conviction in Way is especially strong.

From the beginning, the Way team has shown an unusual combination of technical depth, product judgment, humility, and ambition.

They listen closely to CISOs, but they don’t simply build a collection of customer requests. They use those conversations to refine a clear view of where the market is going and what the architecture needs to become.

They move quickly, challenge their own assumptions, and remain intensely focused on the problem.

That combination matters enormously in a category this complex.

As a seed investor, the greatest privilege isn’t just backing a company before it becomes visible. It is supporting founders while they define a category, sharpen the product, engage early customers, and make the difficult decisions that will shape the company for years to come.

I feel fortunate to be on that journey with the Way team.

And I know this is only the beginning.

Frequently Asked Questions

Why did Glilot invest in Way Security?

There are companies you become excited about because of the market, and there are companies you believe in because of the people. With Way Security, it was both. What made the opportunity so compelling wasn’t just the extraordinary quality of the team, but the scale of the architectural shift they had identified.

What problem does Way Security solve?

Way Security starts from a truth most of the industry ignores: enterprises already own the right identity tools. What’s missing is not another product. It is the ability to enforce those tools on every application and every identity, including the legacy, homegrown, and non-standard systems where enforcement has always broken down.

Why is enterprise identity security fragmented?

For years, identity security has been treated as a collection of separate problems. Organizations deployed one set of tools to manage workforce access, another to govern privileged accounts, another to monitor identity threats, and still others to manage cloud permissions, machine identities, contractors, and third-party access. Each product addressed an important part of the identity problem, but the overall architecture remained fragmented.

How is AI changing identity security?

AI doesn’t create the identity problem, but it dramatically accelerates it. AI agents are being connected to enterprise systems, granted access to sensitive data, and allowed to act on behalf of users and business processes. In many cases, organizations don’t yet have a consistent way to understand what those agents can access, how their permissions interact, or what happens when their behavior changes.

Is the identity security category already won?

The emergence of additional companies lately in this space is meaningful validation, but categories aren’t won by huge marketing campaigns. They are won through architectural clarity, product depth, customer trust, and the ability to turn an ambitious thesis into something security teams can deploy and rely on.

Key Takeaways

- Nofar Amikam led Way Security’s seed investment; the company is now coming out of stealth.

- Identity security has been built as a collection of separate problems, and the resulting architecture remains fragmented.

- AI is making that fragmentation unsustainable: agents are granted access to enterprise systems, and human and machine identities are becoming interconnected.

- Way Security’s premise is that enterprises already own the right identity tools; what is missing is the ability to enforce them on every application and identity.

- For security teams, this means consistent identity controls across the entire environment, without replacing the tools they already trust.